- Source Material: Hana Financial Investment Research Center (Published July 6, 2026)

- Investment Rating & Target Price: BUY / KRW 40,000

- Core Momentum: Margin expansion led by high-value vessel mix, robust backlogs in eco-friendly offshore plants, and entry into the Floating Data Center (FDC) sector.

📊 1. [Valuation Metrics and Financial Indicator Analysis]

Samsung Heavy Industries is demonstrating a structural earnings turnaround amidst a prolonged upcycle in the shipbuilding and offshore industry. Key valuation metrics derived from two-year forward estimates showcase clear improvements in financial quality.

- Market Valuation (Based on 2027 Forecast): The stock trades at a forward PER of 13.92x and a PBR of 2.63x, with an EV/EBITDA of 8.11x.

- Return on Equity (ROE) Trend: ROE is projected to rise from 13.74% in 2025 to 21.04% in the 2026 Forecast and reach 24.11% in the 2027 Forecast.

- Annual Guidance Highlights:

- 2026 Forecast: Revenue of KRW 12,963.7 billion, Operating Profit of KRW 1,509.7 billion

- 2027 Forecast: Revenue of KRW 14,599.5 billion, Operating Profit of KRW 2,021.1 billion

- Short-Term Quarterly Outlook: 2Q26 Revenue is estimated at KRW 3,273.2 billion (QoQ +12.8%) with an Operating Profit of KRW 357.1 billion (QoQ +30.8%), indicating solid structural growth.

🚀 2. [Total Addressable Market (TAM) & Segment Performance Estimates]

The growth engine relies on shifting toward high-margin vessels, expanding highly profitable offshore plant backlogs, and capturing a newly defined coastal infrastructure market.

- Order Backlog Status: As of June 10, 2026, new order intake reached USD 9.6 billion, achieving 69.1% of its annual target (USD 13.9 billion) ahead of schedule. Total order backlog stands solid at USD 35.9 billion, underpinning future revenue recognition.

- Segment Drivers:

- Offshore Segment: Long-term visibility is secured via commercial LNG-related FLNG orders such as Coral and Delfin projects, alongside potential additional orders driven by active FEED biddings.

- Merchant Shipbuilding: Backed by 14 LNG carriers and high-spec tankers, operation optimization including the resumption of Dock 2 will accelerate top-line expansion, steering back-half weighted profitability.

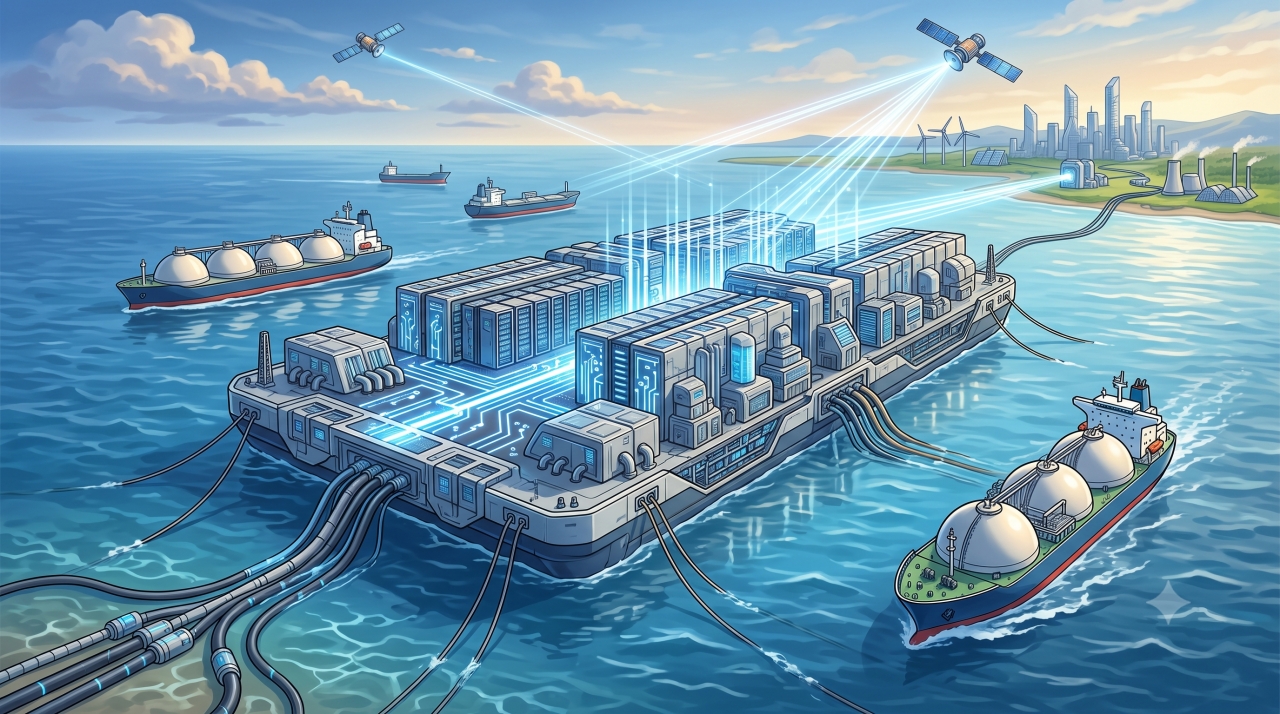

- New TAM Expansion (Floating Data Centers): Floating Data Centers (FDCs) are emerging as a highly profitable market segment. Given that land-based data center construction costs range between KRW 8 billion and 10 billion per MW, coastal FDCs can substantially minimize lead times for licensing and power grid connectivity, promising premium profitability superior to traditional merchant vessels.

📝 Editor Comment

The fundamental thesis for Samsung Heavy Industries is shifting from a conventional heavy manufacturer into a technical maritime infrastructure developer. The projected 2Q26 operating profit margin of 10.9% reflects structurally improved execution despite certain one-off labor cost adjustments. The most vital element to observe is the ongoing project discussions with global US developers regarding FDCs, aiming to address the land-based power shortages and data bottlenecks caused by the global AI infrastructure surge. If these concept-design-certified platforms convert into commercial orders, it will serve as a strong catalyst for multiple re-rating, redefining how the market values the maritime engineering sector.

📢 Disclaimer & Source

- Source: This content has been newly structured and written based on financial facts and numeric data from officially disclosed securities reports.

- Investment Risk Notice: This content is provided for informational and linguistic reference purposes only. Under no circumstances does it constitute financial advice or a recommendation to buy or sell specific securities. All investment decisions and financial liabilities rest entirely with the investor.

- Contact: For compliance and copyright inquiries, please contact ksb220805@gmail.com

🔥 Bulls vs Bears, drop your analysis in the comments!